- The abbreviation for "Debit" is "Dr".

- The abbreviation for "Credit" is "Cr".

- The term debit and credit in bookkeeping and accounting simply denote an increase or decrease to the balance of a referenced business account.

- In double-entry system every business transaction is recorded in at least two accounts, one will be debit entry and another one is credit entry.

- The initial challenge with double-entry is to know which account should be debited and which one should be credited.

- Generally following types of accounts are increased with debit.

- Dividends(Draws)

- Expenses

- Assets

- Losses

- The following types of accounts are increased with credit.

- Gains

- Income

- Revenue

- Liability

- Stockholder's(owner's) Equity

- To decrease an account we do the opposite of what was done to increase to increase the account.

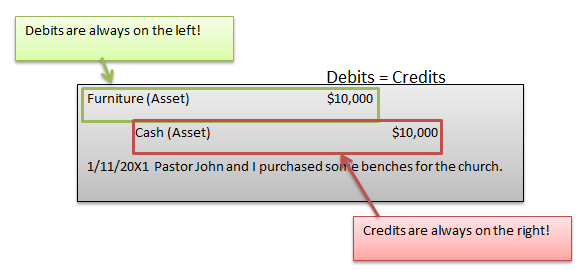

- To debit an account means to enter an amount on the left side of the account.

- To credit an account means to enter an amount on the right side of the account.

Examples: